Claims Process and Fees

Learn How a Public Adjuster Can Help You

When disaster strikes, don't go it alone. Let a Prestige Claim Consultants help you get the most out of your insurance claim.

Public Adjuster Claims Process

Learn How the System Works

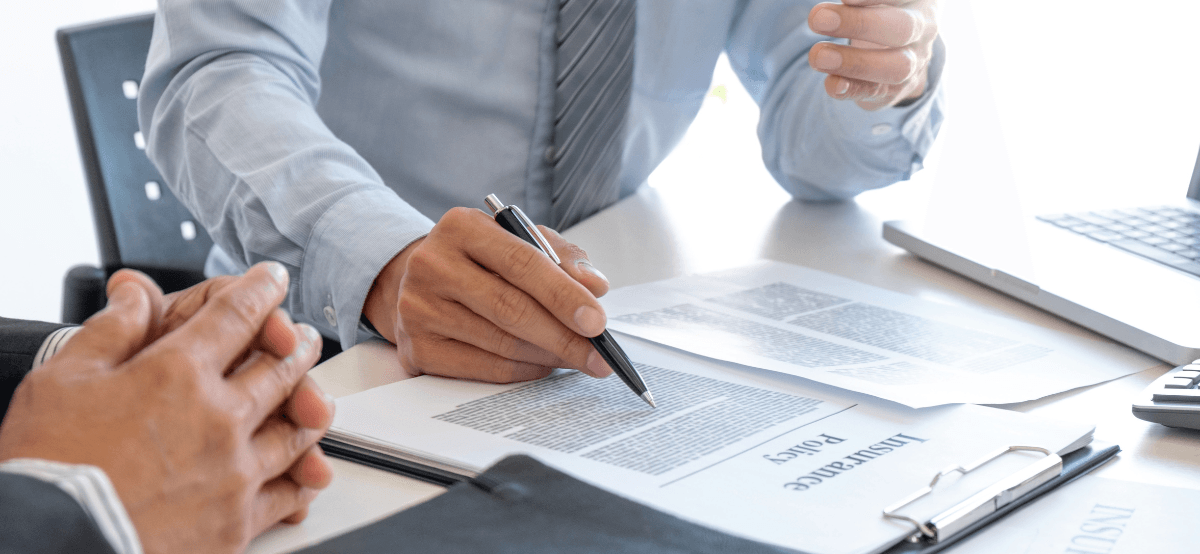

Prestige Claim Consultants, claims process involves an experienced team of advocates who work on behalf of the policyholder to negotiate with their insurance provider.

- It begins with a free no-obligation inspection to determine the extent of damage along with a review of your insurance policy to see if the loss is covered. Once you sign a letter of representation, Prestige Claim Consultants will communicate on your behalf with the insurer.

- We then begin the damage documentation process with photographs, videos, moisture testing, and measuring. Our line item estimates are highly detailed and fully submitted to the insurance company for review. This provides them with a complete understanding of the costs we anticipate for repair and reconstruction.

- The insurance company will then schedule their own inspection. We will be present and work closely with the insurance company adjuster. Thoroughly examining every necessary detail, our goal is to ensure you are adequately represented at your property.

- Once the damages are assessed by the insurance company, negotiations begin. In order to reach a settlement, we need to consult with you, the property owner. Upon obtaining agreement from all parties involved, a release may be signed, and we can move towards receiving a check from the insurance company.

Public Adjuster Fees

We understand that you have a right to remain informed. That’s why we believe it’s important to know how to navigate the insurance claim process and associated fees. As such, public adjuster fees are regulated by the Florida Department of Financial Services to ensure customers understand the cost of service.

Written Contract

Working with public adjusters can be a key part of recovering losses following an incident, however it's important to understand the rules that are in place. Prior to any payments being made, there must exist a written contract between the insurance payee and the public adjuster; only then can they collect on their fee. Please note, an insured or claimant may cancel a public adjuster’s contract to adjust a claim without penalty or obligation within 10 days after the date on which the contract is executed.

Fee Caps

To ensure fairness and protect the client, state laws have set fee caps that govern the compensation public adjusters can accept. It is illegal for public adjusters to receive payments from any source that would exceed the statutory fee cap. Complying with these regulations upholds integrity within the profession and reinforces ethical fiscal responsibility to the customer.

Claim Fees

Public adjusters cannot charge more than 20 percent of an insurance claim payment for claims that are not based on an emergency. They also cannot charge more than 10 percent of the insurance claim payment for claims based on an emergency. These fee limits only apply to residential property insurance policies and condominium unit owner policies. s. 718.111(11), F.S. [See s. 626.854(18), F.S.]

Re-Opened and Supplemental Claims

The fee cap on re-opened or supplemental claims is 20 percent of the claim that is not based on a declared emergency. The 10 percent fee cap for a claim that is based upon a declared emergency still applies as stated above. The public adjuster's fee cannot be based on any payments made by the insurer to the insured prior to the time of the public adjuster contract. These fee caps apply only to residential property insurance policies and condominium unit owner policies. s. 718.111(11), F.S. [See s. 626.854(18), F.S.]

For more information relating to Florida Statutes Regulating Public Adjusters click here.